Deep Dive: Why Housing Costs Keep Rising

To understand why affordability looks the way it does today, you have to understand how housing became a financial instrument in the first place. And the questions only get more difficult from here...

For decades, the majority of middle-income Americans stored their wealth in their homes.

In 1970, a median home cost 2.7x the median household income. By 2024, that figure reached 5.1x. Today, 62% of middle-class wealth sits in an asset that 7 in 10 American households can no longer afford.

Home ownership in the U.S. is now the subject of executive orders, Senate votes, and protest movements. But most of the debate focuses on symptoms rather than the system that created them.

To understand why affordability looks the way it does today, we need to understand how housing became a financial instrument in the first place.

How Homes Became Wealth Storage

For most of human history, a home was just shelter.

The idea that a house should appreciate in value, generate wealth, and serve as the cornerstone of a family’s financial security is a relatively recent concept.

Policy didn’t accidentally inflate housing values. It systematically engineered demand, leverage, and incentives around ownership.

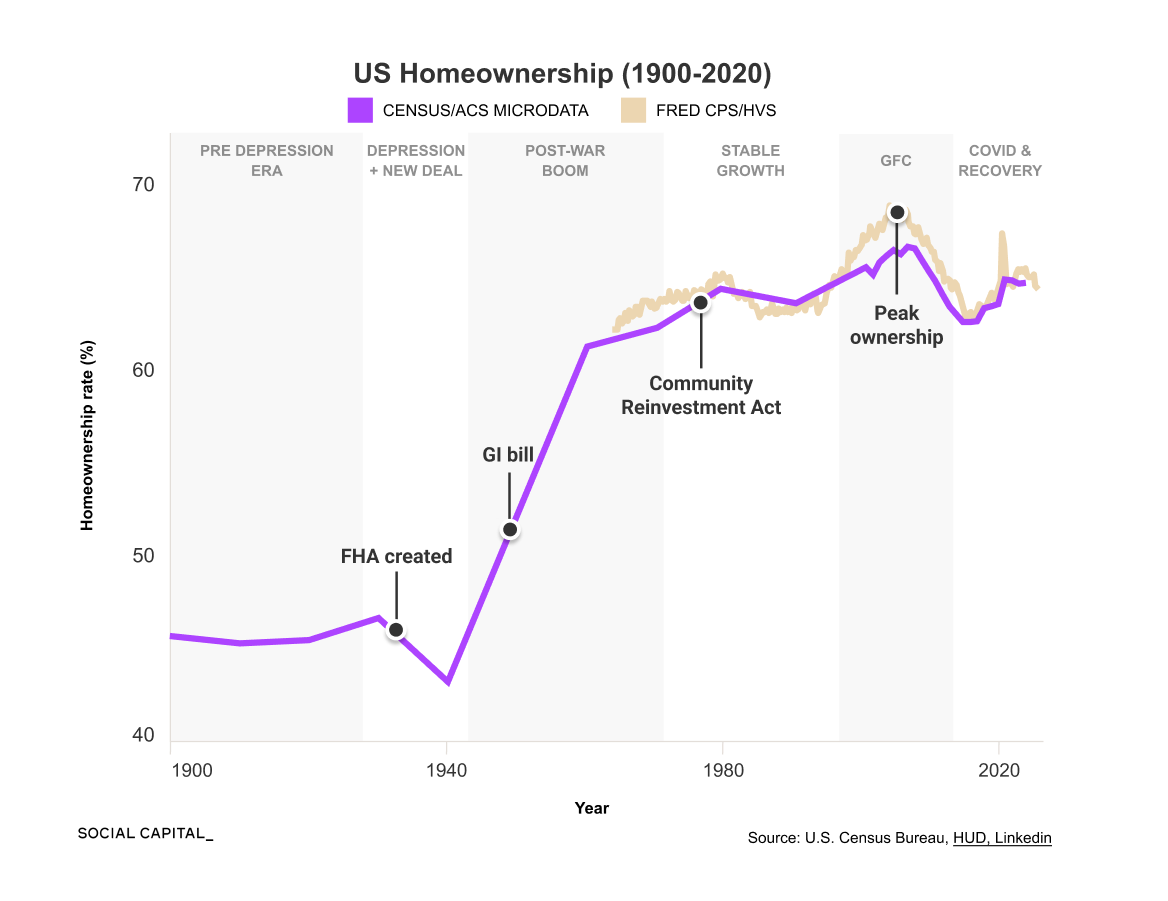

The FHA was created in 1934 to insure mortgages against default. The GI Bill of 1944 extended mortgage guarantees to returning veterans with reduced down payments.

Between 1944 and 1966, one-fifth of all single-family homes built in America were financed with GI Bill assistance, and homeownership rates jumped from 44% to 62%.

Real estate is the only asset class where Americans can routinely borrow 80% to 95% of the purchase price at favorable rates.

A 20% down payment on a $400,000 home gives you control of the full asset with $80,000. If it appreciates 5%, your return on equity is 25%, five times the market gain.

But leverage cuts both ways.

For a buyer who just put 20% down, a 20% price decline wipes out their entire equity position.

When 62% of household wealth depends on a single asset holding its value, every participant in the system, homeowners, local governments, banks, federal policy, is aligned around one outcome: prices must not fall.

That worked for decades. Then the system got tested.

Why The Market Is Freezing

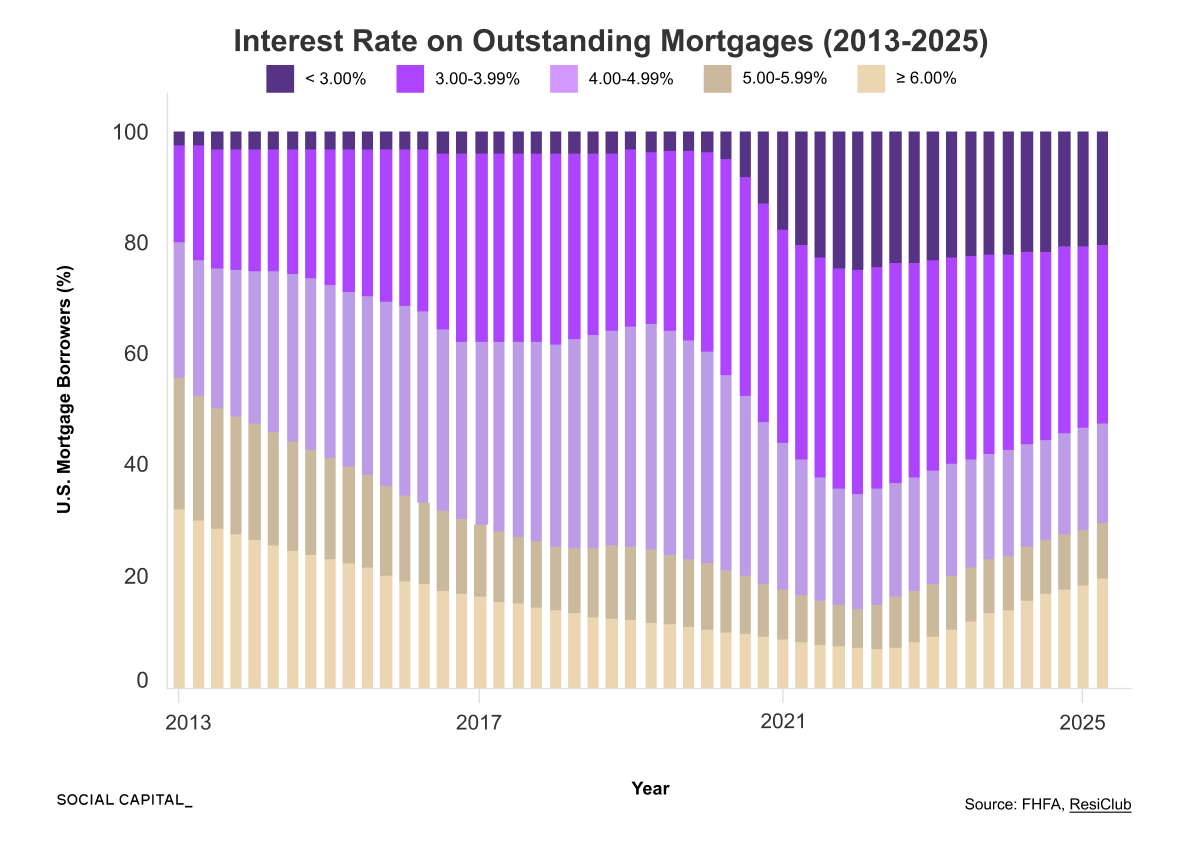

For a decade, near-zero interest rates kept that system running, fueling demand and pushing prices higher. Then in 2022, with inflation running above 9%, the Fed raised rates at the fastest pace in 40 years.

In a normal market, that cools demand, brings prices down, and restores equilibrium. It did cool demand. Active buyers fell from 2.5 million to 1.4 million. But it also killed supply.

Homeowners locked in at 3% faced a $12,000-per-year penalty for selling and buying the same home at 7%. So they stayed put. Demand and supply collapsed at the same time, and prices never came down.

What Fixes Housing Affordability?

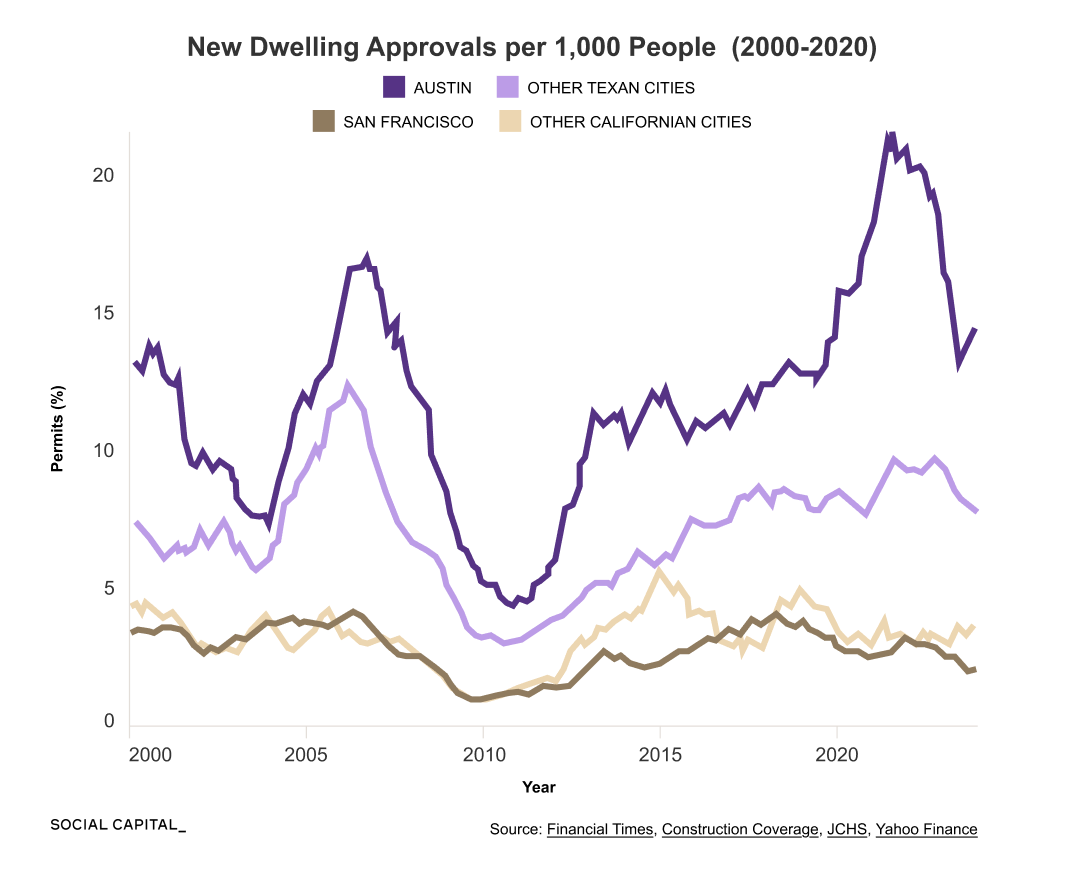

The evidence points to supply.

Austin permitted over 20 units per 1,000 residents at its peak, while San Francisco permitted fewer than 4. Austin’s median home costs about 5x median income. San Francisco exceeds 11x.

The pattern holds across different markets. Places that increase supply through permits and building have more stable prices.

But here’s the trade-off: affordability and wealth-building are in tension. Lower prices help buyers and renters. They hurt the 65% of Americans who already own. And homeowners vote at higher rates, donate more to local campaigns, and show up to zoning meetings.

Every policy choice picks a side. Zoning reform benefits future residents at the expense of current ones. Rent control helps today’s tenants while discouraging tomorrow’s supply.

And the questions only get more difficult from here.

If institutional investors own just 0.5% of single-family homes, why have they become the political villain?

If Houston can permit 6.5 homes per 1,000 residents while Los Angeles permits fewer than 1, is affordability a market failure or a policy choice?

How are phantom mortgages pricing out a generation of buyers before they even apply to purchase a home?

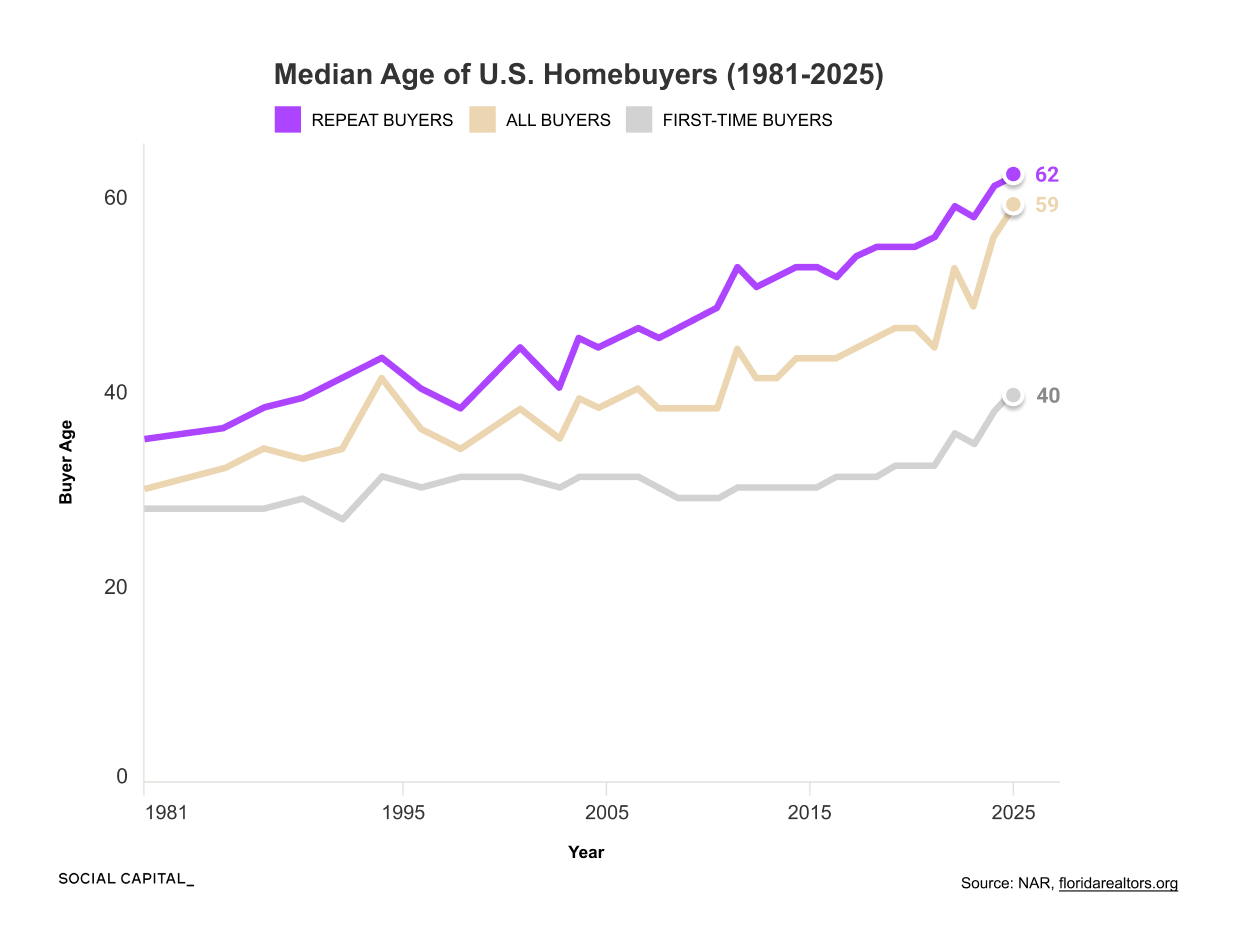

And if only 25% of millennials own a home by 30, compared to 43% of boomers at the same age, is America building a permanent renter class?

Housing affordability sits at the intersection of finance, construction economics, tax policy, demographics, and local politics. Few understand the underlying system that connects each piece.

Our research team at Social Capital spent some time studying housing affordability from first principles and developed a 110-page Deep Dive to bring you up to speed on the system that shapes the most important asset most families will ever own.

Let me know your thoughts in the group after reading.

Chamath

Disclaimer: The views and opinions expressed above are current as of the date of this document and are subject to change without notice. Materials referenced above will be provided for educational purposes only. None of the above will include investment advice, a recommendation or an offer to sell, or a solicitation of an offer to buy, any securities or investment products.

Deep Dive PDF below ↓