SpaceX and Anthropic 300MW Compute Partnership

A summary of the interesting content that I consumed this past week…

What I Read This Week: a summary of the content that I consumed this past week…

Caught My Eye…

1) SpaceX Partners with Anthropic

On May 6, Anthropic signed a multi-year deal with SpaceX to rent the entire compute capacity of Colossus 1, SpaceX’s Memphis supercomputer. The facility gives Anthropic access to more than 300 megawatts of capacity and over 220,000 NVIDIA GPUs, including H100s, H200s, and GB200s. New Street Research estimates the contract will generate $3-$4 billion in annual revenue for SpaceX, with more than $2.5 billion in cash profit.

The deal landed at a time when Anthropic’s capacity constraints had become visibly frustrating for users. Over the past few months, Claude users have been running into tighter limits during peak hours, especially developers using Claude Code. On the same day the deal was announced, Anthropic doubled Claude Code’s rate limits and lifted Opus API input token ceilings massively.

For SpaceX, this becomes a brand-new revenue line. Based on internal leaked memos, xAI’s broader 550,000-GPU fleet had been running at roughly 11% model FLOPs utilization, the share of compute that performs useful work, compared to the 40% standard range. Renting Colossus 1 in full to Anthropic at near-peak utilization turns excess capacity into a multi-billion-dollar line item. Anthropic also mentioned that they are interested in developing multiple gigawatts of orbital AI compute capacity with SpaceX.

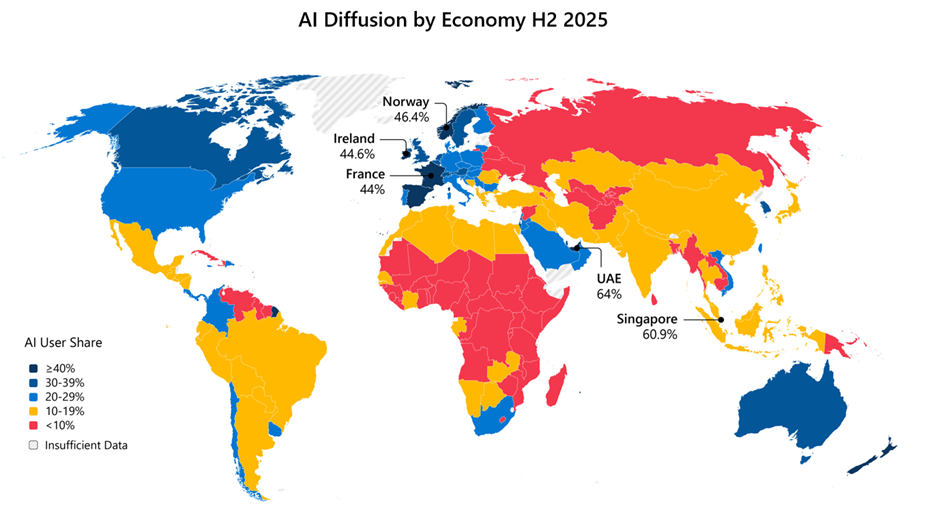

2) The Microsoft Global AI Diffusion Report

On May 7, Microsoft’s AI Economy Institute published its Q1 2026 Global AI Diffusion Report. Use of generative AI is now at 17.8% among the world’s working-age population. Twenty-six economies report adoption above 30%. The UAE leads at 70.1%, and the United States moved up three spots to 21st place, with a usage rate of 31.3% among the working-age population.

AI adoption in the Global North reached 27.5%, while the Global South lingered at 15.4%, and the gap widened by 1.5 percentage points from the second half of 2025 onward.

Microsoft President Brad Smith related this divide to a similar electricity divide that led to disparate economic impacts in the Global North and South. This is why Microsoft announced a $50 billion investment by the end of the decade to help bring AI to countries across the Global South.

Certain parts of Asia is the only region putting up countervailing numbers. South Korea, Thailand, and Japan posted the largest quarterly gains, driven by improved AI performance in Asian languages. The same data shows Git pushes from software developers rose 78% year over year as Anthropic’s Claude Code, OpenAI’s Codex, and GitHub Copilot moved into routine workflow.

3) The Pentagon Picks Its AI Vendors

In the first week of May, three federal decisions touched the U.S. defense AI vendor stack.

On May 1, the Pentagon confirmed that its approved roster of AI vendors for classified Defense Department networks had expanded to eight firms. Google, Microsoft, AWS, NVIDIA, OpenAI, SpaceX, Oracle, and Reflection AI are now cleared to deploy on Impact Level 6 systems, the tier for handling secret information, and Impact Level 7, a new classification for the most sensitive workloads that carries tighter security requirements.

Reflection AI stands out from the list: a two-year-old startup positioning itself as an open-source vendor that has yet to ship a public model. Anthropic was not on the list, having been designated a supply-chain risk earlier this year after declining to grant the Pentagon unrestricted use of Claude for all lawful purposes.

A second layer landed on May 5. The Commerce Department’s Center for AI Standards and Innovation (CAISI) updated its pre-deployment evaluation agreements, adding Google DeepMind, Microsoft, and xAI, while renegotiating existing 2024 agreements with OpenAI and Anthropic under the same framework. CAISI reviews state-of-the-art models before public release, often with safeguards stripped so evaluators can measure raw capability rather than the deployed product. Anthropic, therefore, sits inside the federal evaluation pipeline while remaining outside the Pentagon’s procurement list.

The following day, the Pentagon’s Chief Digital and AI Office (CDAO) raised the ceiling on its Meta-backed Scale AI contract to $500 million for data labeling and decision support, five times the September 2025 award amount.

Across the three decisions, roughly ten firms now make up the visible U.S. defense AI stack, with procurement clearance and safety evaluation only partially overlapping.

4) DeepSeek Takes Its First Outside Money at $45B

On May 6, the Financial Times reported that China’s largest state-backed semiconductor investment vehicle (aka Big Fund) is in talks to lead DeepSeek’s funding round at a valuation of roughly $45 billion. Other major funds, such as Tencent Holdings and Alibaba Group, are also reportedly in talks to co-invest. The round is estimated at $3 to $4 billion.

The company was founded three years ago by Liang Wenfeng as a spin-out from High-Flyer Capital, his quantitative hedge fund. Deepseek was funded entirely from High-Flyer’s balance sheet, allowing Liang to own 89.5% of the company.

The first external round opened in mid-April with a $300 million target at a $10 billion valuation. Within weeks, the implied valuation moved to $45 billion as the Big Fund III, the third phase of the state chip-financing vehicle, entered talks. Proceeds will go to computing infrastructure and staff retention.

The raise comes two weeks after DeepSeek released V4 on April 24, a 1.6-trillion-parameter open-weight model whose Pro variant scored slightly higher than GPT-5.4’s model in Codeforces and matching Opus 4.6 Max on SWE-bench Verified.

Learn With My Friends and Me…

Deep Dive: Where Value Accrues in the AI Stack

How should we think about AI in 2026? The stack we drew has six layers, from the bottom up: infrastructure, chips, data, models, execution, and application. Each layer has its own fulcrum...

Other Reading…

Education Is a Fault Line in U.S. Politics. Democrats Are on the Wrong Side (The 74)

What the Iran War Means for China (Foreign Affairs)

America’s Electricity Gap (Joseph Politano)

On X…

The Pentagon vendor stack and the DeepSeek round are the two items that belong in the same analytical frame because theyre telling you how both superpowers have decided to treat AI, and the answer in both cases is as strategic infrastructure rather than a commercial market.

The Pentagon list is fasinating for what it reveals about the emerging shape of the US defense AI ecosystem. Anthropic declining unrestricted military use and then being designated a supply-chain risk while simultaneously sitting inside the CAISI safety evaluation pipeline is a structural contradiction worth naming. Washington trusts Anthropic enough to evaluate frontier model safety with guardrails stripped but doesnt trust it enough to deploy on classified networks. The company is inside the evaluation layer and outside the procurement layer, which means it shapes the standards that its competitors have to meet without being able to compete for the contracts itself. Thats an extraordinary competitive position that looks like a disadvantage until you think about it for five minutes.

Reflection AI being on the list with no shipped public model is the other signal that deserves scrutiny. A two-year-old startup with zero public track record getting IL-6 and IL-7 clearance tells you the selection criteria for defense AI vendors are not primarily technical. Theyre political and relational. The approved roster is a map of who has relationships inside the Pentagon, not a ranking of who has the best models.

The DeepSeek round at $45B changes the competitive landscape structuraly. When Chinas largest state semiconductor investment vehicle leads a funding round, the line between commercial AI and state-directed AI infrastructure disappears entirely. Liang Wenfeng owned 89.5% of the company before this round. After Big Fund III enters, the state has a seat at the table and the distinction between DeepSeek the startup and DeepSeek the national champion becomes semantic rather than operational.

The speed of the valuation jump matters too. $10B in mid-April to $45B by early May is a 4.5x repricing in three weeks. That velocity tells you the state actors involved arent price-sensitive. Theyre buying strategic positioning, not financial returns. The same way the US government bought 10% of Intel for strategic reasons rather than investment returns.

The convergance of both stories points to a specific conclusion about where the AI competition is heading. Both governments are now treating AI labs as extensions of national security infrastructure. The commercial market for frontier AI is quietly becoming a regulated defense market with commercial customers as a secondary consideration. The companies that navigate this transition successfully will be the ones that understand they are now defense contractors who happen to have consumer products, not consumer tech companies who occasionally sell to the government.

Wait a second, if anthropic is renting colossus what's left for grok? I thought grok was using colossus?